Truckload spot rates hit an all-time record high in early June 2026, jumping $0.09 per mile overnight to $3.83 per mile, the highest level ever recorded (FreightWaves, 2026). Tender rejections, a key signal of how often carriers are turning down contracted loads, climbed to 17.55% (FreightAlley, 2026). And according to the Logistics Managers Index, transportation prices are expanding at “the fastest rate of expansion ever recorded for any metric in the nearly ten-year history of the index” (LMI, May 2026).

Transportation continues to move at a significant pace. Transportation Prices are up (+1.0) to 96.0, which is the fastest rate of expansion ever recorded for any metric in the nearly ten-year history of the index. Transportation Capacity continues to contract quickly at 31.7, and Transportation Utilization expansion remains elevated at 69.5. The transportation market has been tight, with prices growing at an unprecedented rate since the closure of the Strait of Hormuz. (LMI, May 2026).

This is a structural shift mostly impacted on the supply side and understanding what is driving pricing higher will determine whether your transportation budget survives 2026 intact.

What Is Happening in the Freight Market Right Now

Spot Rates at Historic Highs

Van load-to-truck ratios on DAT are up 92% year-over-year. Flatbed load-to-truck ratios are up an extraordinary 189% year-over-year (DAT Trendlines, 2026). The load-to-truck ratio measures the number of available freight loads posted for every available truck, a higher number means more freight is competing for fewer trucks, and rates reflect that immediately.

On the supply side, truck postings are down 22.7% year-over-year. While on the demand side, load postings are up 64.9% (DAT Trendlines, 2026). That is a structural imbalance on the supply side which is pushing prices higher.

HedgeEye has also confirmed that U.S. trucking rates have surged to the highest levels since 2022 (HedgeEye via FreightAlley, 2026). Critically, this rate spike is happening even as fuel prices have cooled week over week. That matters because it proves the inflation in rates is being driven by supply-and-demand dynamics in the carrier market itself, not because of fuel cost pass-through.

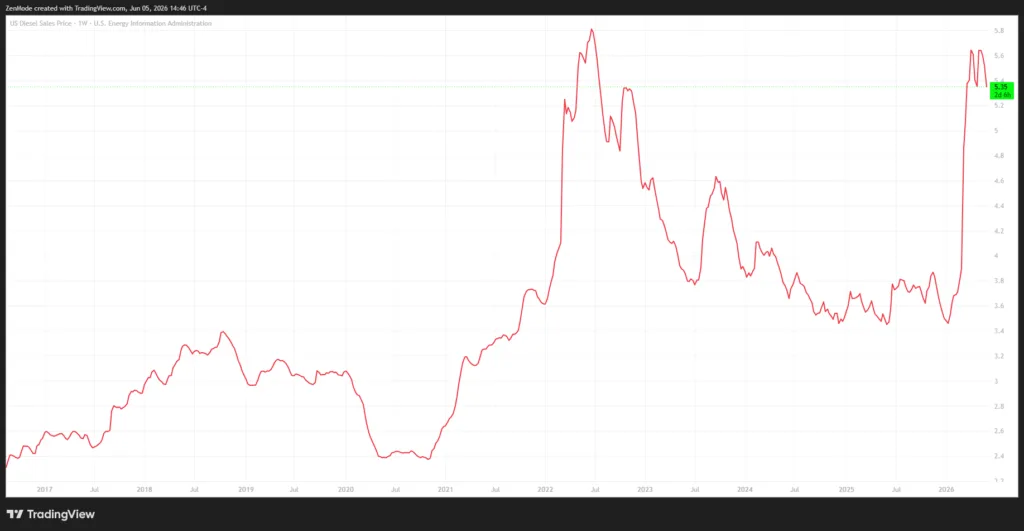

Diesel is Still Elevated

Even with some recent relief, diesel prices remain a major cost factor. The national average diesel price is $5.350 per gallon according to the U.S. Energy Information Administration, up $1.899 year-over-year. California is seeing $7.051 per gallon and the New England region is at $5.731 per gallon (EIA, June 2026).

The FMCSA Crackdown: Why Tens of Thousands of Drivers Are Being Removed

This is the story that is reshaping the freight market more than anything else. The Federal Motor Carrier Safety Administration (FMCSA) has launched the most aggressive enforcement push in my 16-year career serving this industry.

Craig Fuller, the esteemed CEO of FreightWaves, one of the most closely watched transporation news outlets in the industry, stated directly: “The compliance crackdown has already created the hottest spot market in history. 40,000 non-compliant drivers have been eliminated. There could be hundreds of thousands more being taken out in coming months and years.” (FreightAlley, 2026).

The enforcement actions include:

- English-language proficiency rules: 20,000 drivers have been knocked out-of-service for failing to meet English-proficiency requirements (USDOT, 2026).

- Illegal CDL revocations: 28,000 illegally issued commercial drivers’ licenses for unqualified foreign drivers have been revoked (USDOT, 2026).

- Non-domiciled CDL enforcement: Stricter scrutiny of drivers holding commercial licenses from states where they do not legally reside.

- Drug Clearinghouse enforcement: Increased use of the federal database tracking drivers with drug and alcohol violations.

- MOTUS registration system: FMCSA sent 2.2 million letters to all registered motor carrier addresses when it launched the new Motus carrier registration system. Over 400,000 of those letters came back as undeliverable, meaning those carriers cannot be verified or contacted (SuperTrucker via X, 2026).

States are also taking independent action. Indiana now requires CDL skills tests to be conducted in English and mandates proof of legal work authorization. Approximately 2,000 licenses were affected when the law took effect in April 2026 (Indiana Capital Chronicle, 2026).

The FMCSA’s new leadership has been described by FreightWaves as a regulator who “shows up”, a sharp contrast to prior years. The agency is signaling that this is the beginning of enforcement, not the end (FreightWaves, 2026).

The Supreme Court Ruling That Changes Everything for Shippers and Brokers

In a unanimous decision, the U.S. Supreme Court ruled that the Federal Aviation Administration Authorization Act (FAAAA) does not protect freight brokers from state-law negligence claims when they hire unsafe motor carriers. This ruling came out of the Montgomery v. Caribe Transport II case and has sent shockwaves through the brokerage industry (ZeroHedge, 2026; FreightWaves, 2026).

What does this mean?

Freight brokers, and shippers can now be sued under state law if they negligently hire a carrier that causes harm. Previously, big box brokers had argued that federal law shielded them from those claims.

But here is what shippers must understand: the same logic applies to them.

As one industry analyst noted, plaintiff attorneys are already signaling they will pursue shippers directly for carrier safety underwriting failures: “A shipper has the same access to public safety information as a broker, and this will be argued in court” (FreightAlley, 2026). Triumph Financial CEO Aaron Graft put it even more bluntly: “The era of choosing the closest, cheapest truck is officially over. Today, freight selection is a high-stakes legal exercise” (FreightWaves via X, 2026).

For shippers who handle their own carrier selection, particularly those without structured vetting processes, carrier vetting technology, or compliance workflows, this is an exposure that needs immediate attention. The most practical response we are hearing is that many shippers are already making: delegating carrier sourcing to qualified managed logistics providers with rigorous vetting processes. When done with the right vendor, it provides processes and technology exhibing evidence of due diligence, which matters enormously if litigation ever arises.

How Much Capacity Is Actually at Risk

This is where the numbers get alarming. Craig Fuller offered this breakdown: approximately 1.2 million trucks, representing 36% of the fleet, have no safety rating from the FMCSA. An additional 300,000 trucks carry a “conditional” safety rating, which is the category regulators and courts are treating as the riskiest to load (FreightAlley, 2026). That is 1.5 million trucks that responsible brokers and shippers can no longer confidently use if they want to demonstrate due diligence.

To understand the scale: the compliance crackdown removed approximately 40,000 trucks from service since last June, and spot rates have already hit all-time highs. If brokers and shippers begin refusing conditional carriers at scale, which is now occurring, the capacity reduction would be larger than any event in the history of the industry. It is worth briefly advising that TLI has already had a strict policy in place prohibiting the use of conditional carriers, the entire industry is largely following along now into best practices. As far as this capacity reduction Fuller called it directly: “Welcome to the trucking super cycle” (FreightAlley, 2026).

Overall Transportation Capacity is contracting a bit slower (+3.3), but at a still rapid pace of 31.7. (LMI, May 2026).

Insurance costs compound this increase in costs. The TIA (Transportation Intermediaries Association) President Chris Burroughs has indicated that insurance costs for freight brokers and 3PLs may increase by five times in the wake of the Supreme Court ruling (FreightWaves, 2026). Those costs flow downstream, into freight rates, into accessorial surcharges, and into the total cost shippers pay per shipment.

Demand Is Growing, Too. Folks, this isn’t just a supply story anymore

While much of the focus has been on the supply side of the market, demand is accelerating. The ISM Manufacturing PMI reached 54.0 in May 2026, the fifth consecutive month of expansion and the highest reading since May 2022 (ISM, 2026). A PMI above 50 indicates expansion. New orders, production, and backlog of orders all grew faster. Customer inventories are rated as “too low,” which historically precedes a wave of restocking freight.

Manufacturing is being driven in part by a remarkable run in AI data center construction, energy infrastructure, and military production, all freight-intensive sectors that favor flatbed and specialized equipment.

Rail is surging alongside trucking. U.S. rail traffic increased 7.2% year-over-year to 492,795 carloads and intermodal units for the week ending May 30, according to the Association of American Railroads (Progressive Railroading, 2026). This tells you demand pressure is not isolated to one mode, it is systemic.

The LMI also flagged that transportation capacity is “contracting quickly” at an index reading of 31.7, while transportation utilization remains elevated at 69.5 (LMI, May 2026). The LMI’s author described current conditions as a “meteor shock” event, not an incremental tightening, but a sudden and severe disruption.

Why This Market Is Tighter Than 2022

Many shippers remember 2022 as a painful but temporary capacity crunch. There is a critical difference with what is happening now.

The 2022 crunch was demand-driven. As exhibited in prior analysis, the pandemic-era inventory demand and a surge in consumer spending hit the market simultaneously. Once demand normalized, the market loosened quickly. Excess capacity flooded back in along with the supply of trucking capacity increasing.

The current market is supply-side structural. The carriers being removed are not coming back. Drivers who lose their CDLs do not re-enter the system next quarter. Enforcement that tightens the carrier pool does not reverse when the economy softens. And new regulatory requirements, including proposed legislation (H.R. 8870) that would require certified officers at freight brokerage firms, will further shrink the pool of qualified intermediaries over time. Supply-side capacity problems take years to resolve, not quarters.

Where Freight Costs Are Actually Accumulating

Many transportation directors look at total freight spend as their primary metric. That is a mistake in this market. Total freight spend is too blunt of an instrument. It tells you what happened, but not why it happened, and it cannot show you where the real problems are building.

In a market like this, cost pressure increases because the carriers can administer their fees more forcibly. Here is where it actually accumulates:

- Detention charges when facilities are not moving trucks efficiently

- Accessorial fees that spike when carriers have pricing power

- Routing guide failures when your contracted carriers reject loads and you are forced onto the spot market. Tender rejects are currently already above 17%!

- Short lead-time shipments that almost always will be priced at a significant premium

- Service failures that cause expedited shipments and premium freight costs

- Unplanned spot market utilization that blows through rate budgets

The companies managing freight costs best right now have delegated their transportation to a logistics management company that is monitoring supply chain activity at the shipment level: tender acceptance rates by carrier, unique custom contracting, custom fuel tables, dwell time by facility, lane-by-lane execution consistency, and spot utilization versus old-school static routing guides. In addition, inbound vendor routing is another area where costs accumulate largely unnoticed. Many shippers have limited visibility into how their vendors are selecting carriers and routing inbound freight, often without fielding the transportation routing through a dynamic rating engine that optimizes the least cost provider utilization, and those choices directly affect total delivered costs.

At TLI we have visibility into their freight data at a granular level. We take carrier vetting seriously, and we are not over-concentrated in any single carrier relationship, and we exceed at executing freight strategies proactively rather than reacting to rate spikes.

Transportation is no longer simply a matter of “service + market rates” it has become a legal exercise, a compliance function, and a strategic variable all at once.

References:

DAT TrendLines. (2026). Load-to-truck ratios and posting data. https://www.dat.com/trendlines

FreightAlley [@FreightAlley]. (2026, May). Craig Fuller commentary on FMCSA crackdown and tender rejections [Posts]. X. https://x.com/FreightAlley/status/2057997250886766670?s=20; https://x.com/FreightAlley/status/2062843900755091600?s=20; https://x.com/FreightAlley/status/2056701966680572178?s=20; https://x.com/FreightAlley/status/2055633238756933670?s=20; https://x.com/FreightAlley/status/2057544058135019744?s=20; https://x.com/FreightAlley/status/2055624667600138314?s=20

FreightAlley [@FreightAlley]. (2026, June). Spot rates approach all-time highs [Post]. X. https://x.com/FreightAlley/status/2062677770740572517?s=20

FreightWaves. (2026). The FMCSA finally has a regulator who shows up and the freight market is responding. https://www.freightwaves.com/news/the-fmcsa-finally-has-a-regulator-who-shows-up-and-the-freight-market-is-responding

FreightWaves. (2026). Post-Montgomery focus grows on fate of 3PL insurance premiums. https://www.freightwaves.com/news/post-montgomery-focus-grows-on-fate-of-3pl-insurance-premiums

FreightWaves. (2026). Trucking is driving double-digit growth for this rail freight category. https://www.freightwaves.com/news/trucking-is-driving-double-digit-growth-for-this-rail-freight-category

FreightWaves [@FreightWaves]. (2026). Triumph Financial CEO Aaron Graft on carrier liability [Post]. X. https://x.com/FreightWaves/status/2061895643765862801?s=20

Highway. (2025). Translogistics Inc. (TLI) partners with Highway to elevate carrier vetting and secure sensitive shipments [Press release]. https://highway.com/press-releases/translogistics-inc-tli-partners-with-highway-to-elevate-carrier-vetting-and-secure-sensitive-shipments

Indiana Capital Chronicle. (2026, February 24). Indiana senate adds English-language CDL testing, immigration checks to trucking bill. https://indianacapitalchronicle.com/2026/02/24/indiana-senate-adds-english-language-cdl-testing-immigration-checks-to-trucking-bill/

Institute for Supply Management. (2026, May). Manufacturing ISM report on business. https://www.ismworld.org/globalassets/pub/research-and-surveys/rob/pmi/irun202605pmi.pdf

Logistics Managers Index. (2026, May). May 2026 Logistics Managers Index. https://www.the-lmi.com/may-2026-logistics-managers-index.html

U.S. Congress. (2026). H.R. 8870, 119th Congress. https://www.congress.gov/bill/119th-congress/house-bill/8870/text

U.S. Department of Transportation [@USDOTRapid]. (2026). CDL enforcement actions [Post]. X. https://x.com/USDOTRapid/status/2056835857772855418?s=20

U.S. Energy Information Administration. (2026, June). Weekly retail gasoline and diesel prices. https://www.eia.gov/petroleum/gasdiesel/

U.S. Federal Motor Carrier Safety Administration. (2026, May 26). Waiver for the transportation of fertilizer products in select states. https://www.fmcsa.dot.gov/sites/fmcsa.dot.gov/files/2026-05/Waiver%20For%20The%20Transportation%20Of%20Fertilizer%20Products%20In%20Select%20States.pdf

SuperTrucker [@supertrucker]. (2026). FMCSA Motus undeliverable letters [Post]. X. https://x.com/supertrucker/status/2057962826447167813?s=20

ZeroHedge. (2026). American freight revival enters next phase as illegal alien trucker chaos continues. https://www.zerohedge.com/political/american-freight-revival-enters-next-phase-illegal-alien-trucker-chaos-continues

Spot rates hit record levels in June 2026 due to a combination of supply-side capacity tightening and rising freight demand. Regulatory enforcement by the FMCSA has removed tens of thousands of non-compliant drivers and carriers from service. At the same time, manufacturing demand is expanding, the ISM PMI reached 54.0 in May, creating more freight competing for fewer trucks.

The load-to-truck ratio measures how many available freight loads are posted for every available truck on a given market or lane. When the ratio rises, carriers have pricing power because demand exceeds supply. As of mid-2026, the van load-to-truck ratio is up 92% year-over-year and the flatbed ratio is up 189%.

The FMCSA (Federal Motor Carrier Safety Administration) has launched aggressive enforcement of existing trucking regulations, including English-language proficiency requirements, illegal CDL revocations, and a new carrier registration system called MOTUS. Approximately 40,000 non-compliant drivers have already been removed from service, and enforcement officials have indicated the effort is only in its early stages. Fewer compliant carriers means tighter capacity and higher rates.

The Supreme Court ruled that freight brokers can be sued under state law for negligently hiring unsafe carriers. Industry attorneys have indicated that shippers face the same exposure, since they have access to the same public safety data as brokers. Shippers who work carrier direct and select carriers without documented vetting processes, technology and tools now face legal liability if an unsafe carrier was tendered a load and causes harm.

Mid market shippers often need more than a freight broker. They need a managed transportation provider that can reduce transportation costs, improve carrier performance, provide shipment visibility, and support long term growth. TLI delivers these capabilities through its managed transportation services and ViewPoint TMS platform.

A conditional safety rating from the FMCSA indicates a carrier has safety deficiencies. It is the category most at risk of legal challenge if something goes wrong. Approximately 300,000 trucks in the U.S. carry this rating. Working with those carriers, particularly after the Supreme Court ruling, creates measurable legal exposure. Because of this, TLI has had a long-standing rule prohibiting the use of conditional carriers.

The 2022 crunch was demand-driven and resolved when consumer spending normalized. The current market is a supply-side structural issue driven by regulatory enforcement, carrier exits, and legal liability changes. Supply-side constraints resolve much more slowly than demand cycles, and the capacity that has already been removed is not coming back.

Working with a qualified freight broker that vets carriers rigorously provides both capacity access and legal protection.